Sector: Consumer Discretionary

Size: Large-cap

Website: http://www.chipotle.com

A "messy" recent history: In the last few months, Chipotle has had a bad case of burrito indigestion (chipotle.com). Five incidents of outbreaks have been reported (WSJ):

"Since July, there have been a total of five outbreaks linked to Chipotle, including a little-reported case of E. coli that sickened five people in Seattle and which was a different strain unrelated to the larger outbreak that began in October, as well as a norovirus case in Southern California, a salmonella outbreak in Minnesota and the Boston [norovirus] outbreak."

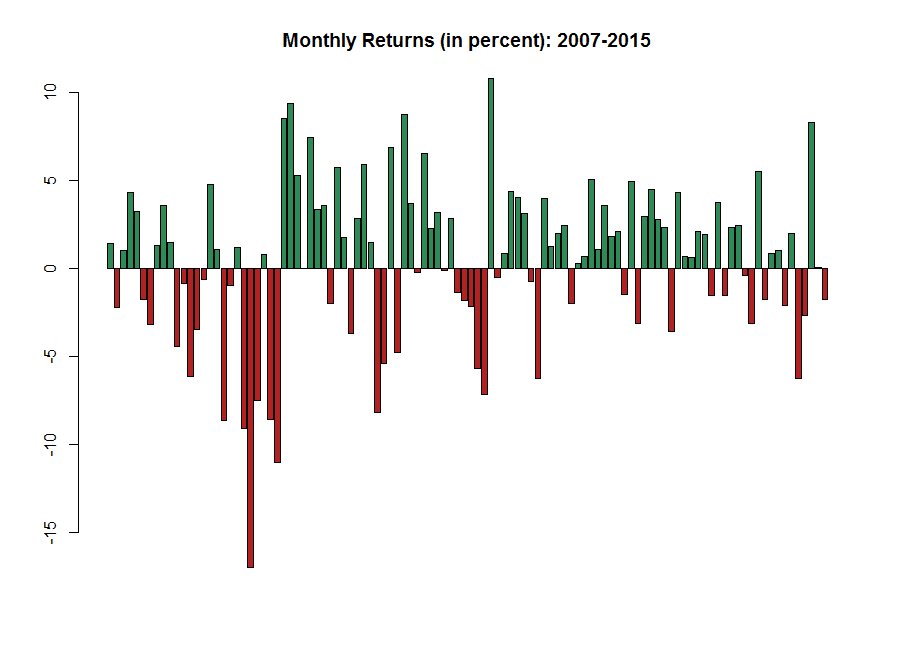

From a close of $720 in September 2015, the stock closed at $448 yesterday, a fall of 38 percent. Its stock chart is a mess -- though the downward momentum of the fourth quarter of 2015 seems to have abated:

Not surprisingly, analysts have ratcheted down their earnings per share estimates sharply. For the fourth quarter of 2015, estimates have fallen 57 percent from $4.37, ninety days ago, to $1.86 today. For 2016, estimates have fallen 37 percent from $20.46, ninety days ago, to $12.86 today (Yahoo! Finance).

In terms of earnings per share, roughly, 2016 represents a setback of 2.5 years.

The Business: Chipotle sells burritos, tacos, burrito bowls, and salads -- "a few things, thousands of ways" -- at its more than 1,900 fast casual restaurants, primarily in the U.S. The company also operates a much smaller chain of 11 Southeast Asian Kitchen restaurants and invests in an entity that operates 3 Pizzeria Locale restaurants. The company's by-line is "food with integrity." Its grander aim is to change "the way people think about and eat fast food."

Risks: After the outbreaks, will consumers return? According to the company, same restaurant sales fell about 15 percent in the fourth quarter of 2015 (Bloomberg). Nevertheless, I believe consumers will eventually return. With good, honest companies, the underlying business eventually recovers. In the 1980s, Johnson & Johnson had the Tylenol scare. They fixed it. Consumers returned. A few years ago, Johnson & Johnson had problems with manufacturing. They fixed it. Consumers returned. Where there is value -- and integrity -- in the brand, as with Johnson & Johnson and Chipotle; and problems are addressed, as Johnson & Johnson did and Chipotle is doing (chipotle.com), consumers do eventually return.

Of the other risks, commodity costs are one. Consumers do visit restaurants less often during recessions -- though Chipotle's relatively inexpensive food may mean it may not see the dramatic declines symptomatic of higher-priced restaurants.

Few other risks, longer term, meaning, in the next 10 or so years.

The Numbers: Profit margins have averaged ten percent the last five years. Asset turnover is 1.6. Chipotle does not have long-term debt -- in the traditional sense. It does, however, disclose deferred rent obligations. Financial leverage is low, 1.3. Return on equity is 22 percent. Likewise, return on equity has averaged 22 percent the last five years. Moreover, because the company has excess cash and investments on its balance sheet, its "true" return on equity is higher.

Dividends and Share Buybacks: The company does not pay a dividend. The company does buy back shares, mostly, it seems, to offset dilution. Over the last five years, the company has retired its shares at a modest 0.4 percent per year clip. (Comparatively, dividend growth stocks typically retire their shares at a much higher rate, but Chipotle is a high-growth stock. In fact, that it even retires its shares is somewhat of a bonus.)

Spreadsheet Parameters: (I use the spreadsheet described in Investing in Dividend Growth Stocks (Amazon) -- with a slight tweak to adjust for the possibility of a robust recovery in earnings per share -- to value the stock. See pages 158 - 176.) Actual dividend payout ratio of 0 percent; assumed payout ratio of 35 percent. Return on beginning equity: 30 percent. It is currently 29 percent. It has averaged 27 percent the last five years. In fact, because the company has excess cash and investments on its balance sheet, its "true" return on beginning equity is higher -- I am likely conservative with my 30 percent. Earnings growth has averaged an impressive 29 percent the last five years. Few large companies can sustain such high growth rates over long periods and, in that sense, Chipotle is one of the rare ones. Dividend growth: n/a. Earnings per share growth roughly mirrors earnings growth because share buybacks are muted. Chipotle operates more than 1,900 restaurants. The company opens more than 200 net new restaurants a year. It is not unreasonable to assume they can maintain this pace for at least the next several years. I do not believe the market is near saturation. For instance, McDonald's is virtually everywhere in the U.S. -- and McDonald's has 14,300 U.S. restaurants (though they do intend to close a handful this year (New York Times)). Moreover, Chipotle will almost certainly expand outside the U.S. more aggressively at some point and the company is testing a few new restaurant ideas. Reasonable growth rates for our spreadsheet, if sales were to resume their historical growth rates: (Years 1-5: 26 percent) (Years 6-10: 22 percent) (Years 11-20: 16 percent) (Years 21-30: 10 percent) (Years 31+: 3 percent).

Sample Spreadsheet Results: Because earnings per share can vary dramatically the next several quarters, I use four potential scenarios to gauge the scope of variability:

- (1) Reset -- current depressed earnings per share.

- (2) Quick Reset -- higher current earnings per share.

- (3) Reset ++ -- current depressed earnings per share, then full recovery next year.

- (4) Quick Reset ++ -- higher current earnings per share, then full recovery next year.

Explicitly, I use the following values:

| Scenario | Stock Price | EPS - current | P/E ratio - current | EPS - next |

| (1) | 450 | 11 | 41 | 13.86 |

| (2) | 450 | 15 | 30 | 18.90 |

| (3) | 450 | 11 | 41 | 22.55 |

| (4) | 450 | 15 | 30 | 22.55 |

These earnings per share are for periods centered on January 1 -- thus the last 6 months of 2015 plus the first 6 months of 2016 for the current period, for example.

Of course, even within these patterns, we have many other possibilities -- but at least they help establish a range. Using a current stock price of $450, and the spreadsheet described in Investing in Dividend Growth Stocks (Amazon), I get the following results:

| Scenario | Expected Return |

| (1) | 12.33% |

| (2) | 13.85% |

| (3) | 14.80% |

| (4) | 14.79% |

Screenshots from the spreadsheet for scenario (3), also showing the slight tweak in red (also needed in scenario (4)) I made in the Projections section:

These are long-term returns. All are outstanding -- because growth remains deliciously high. If Chipotle produces these gains, investors will be well ahead of the market. That said, none of these results make any sense if growth permanently collapses (YouTube) but I do not believe this happens.

In addition, risk is not low under any of our scenarios -- as the relatively high P/E ratios attest.

As a comparison, if we were to live in a parallel universe (YouTube), with the recent company-specific indigestion nonexistent and Chipotle humming along, at a stock price of (say) $600 (to account for the recent market decline -- the market still declines in the parallel universe) and earnings per share of $19, all other assumptions the same as above, the expected return is 13.59 percent a year -- and, yes, with a P/E ratio of 32, the stock is still not low risk. Blame those high P/E ratios -- even in the parallel universe.

Disclosure: I own a tiny position in Chipotle, entirely for fun. I always order a carnitas burrito. It rocks. Do not interpret this post as a recommendation to buy or sell or trade or whatever, including buying a Chipotle burrito. Always do -- and depend -- on your due diligence.